by Dedra Murchison | Oct 29, 2013 | Past, Present, Tips

Does anyone remember Black Tuesday? It was the day that marked the beginning of the Wall Street Crash of 1929. Eighty-four years ago today, we were on the brink of the Great Depression. We call it the Great Depression – not because it was good but because of the...

by Dedra Murchison | Oct 11, 2013 | Change, Choice, Future, Present, Tips

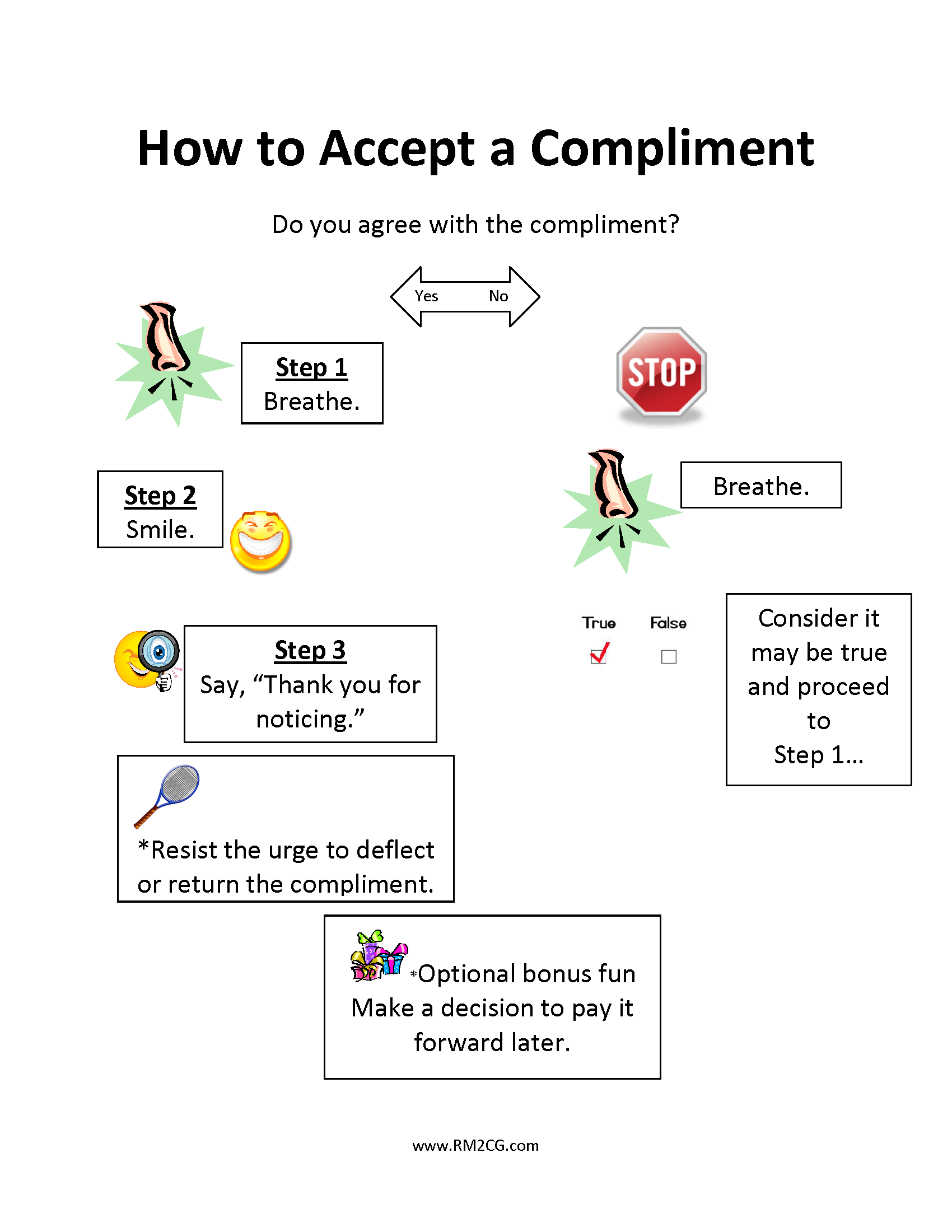

I can take criticisms but not compliments- James Taylor Someone compliments you for the outfit you are wearing or a job well done. Your typical response is: a) “Thank you for noticing.”b) “Oh it was nothing – anyone with a pulse could...

by Dedra Murchison | Oct 10, 2013 | Financial Planning, Goals, Tips

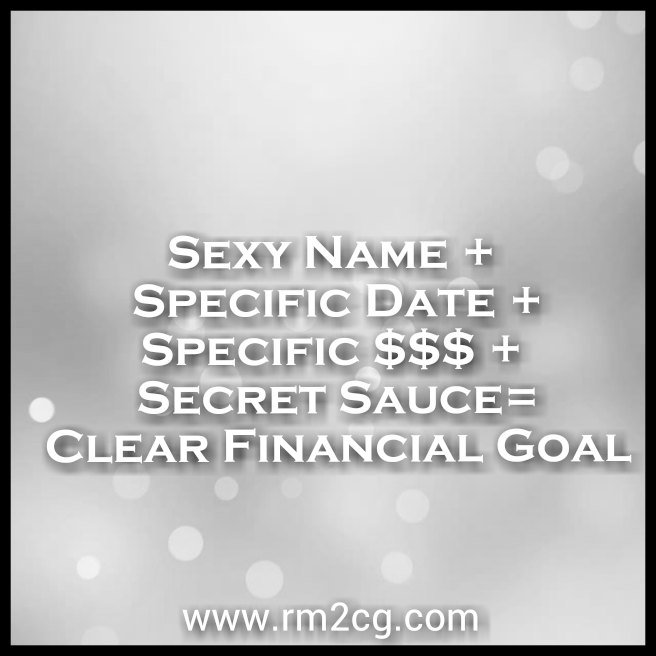

In our last post, we talked about the first three steps to creat clear financial goals. Today, we are going to reveal the last three steps AND the secret sauce ingredient…. Step 4 of Goal Setting 101 – Add the secret sauce. Imagine that it is the date...

by Dedra Murchison | Oct 9, 2013 | Financial Planning, Goals, Tips

You know about SMART Goals. You even know about SMARTER Goals. But do you know how to create clear financial goals? <cue drum roll> GOAL SETTING 101 Formula I am about to show you the secret to creating clear financial goals. Are you ready? Step 1 of Goal...

by Dedra Murchison | Oct 8, 2013 | Budget, Change, Choice, Financial Planning, Money Story, Present, Spending Diary, Spending Plan, Tips

Reason #1 to use a spending diary You have more month at the end of your money. Spending diaries are a tool to help you track your spending. Reason #2 to use a spending diary You have a high debt to income ratio. Studies show that when people pay with cash, they spend...

by Dedra Murchison | Oct 4, 2013 | Change, Choice, Money Story, Past, Present, Tips

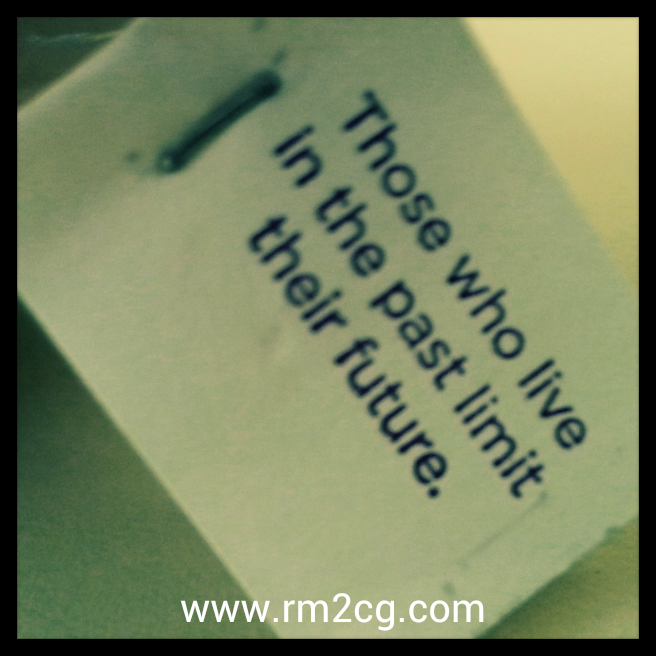

Past performance is not indicative of future results… This standard disclaimer applies to many investment vehicles. It typically does not apply to human behavior. We are creatures of habit and tend to do the same thing – even when it becomes...